This article is a continuation of the article I wrote last week which can be found here .

My favorite startup author, Eric Ries, write some very interesting points for corporate innovators in his book ‘the startup way’. He explains what makes silicon valley startups special. In bigger enterprises that try to build innovation programs or corporate startups, leaders can use these ideas to create the right culture and structure. Let’s have a look at some of the characteristics of startups:

Part 1

- It’s all about the team

- Small teams are better than big teams

- Every team has a cross-functional structure at its core

- Every project starts with the customer in mind

- Silicon valley startups have a specific financial structure

Part 2

- We focus on leading indicators

- Metered funding stages risk

- Board/investor Dynamics are key

Part 3

- We believe in meritocracy. Unlike in a corporate setting, where everything has to be right in order to proceed, a startup doesn’t need to have everything figured out yet.

- Our culture is experimental and iterative

- We believe in entrepreneurship as a career choice

In this article, we will look at part 2 of the above factors.

We focus on leading indicators

This is one of the most important elements of startup-investment: what metrics show real progress? The answer to that question varies between stages of the startup life-cycle. In Eric’s own words:

Implicit in this focus on metrics is a clear understanding of the difference between trailing indicators (such as gross revenues, profit, ROI and market share) and leading indicators that might predict future success (such as customer engagement, satisfaction, unit economics, repeat usage, conversion rates).

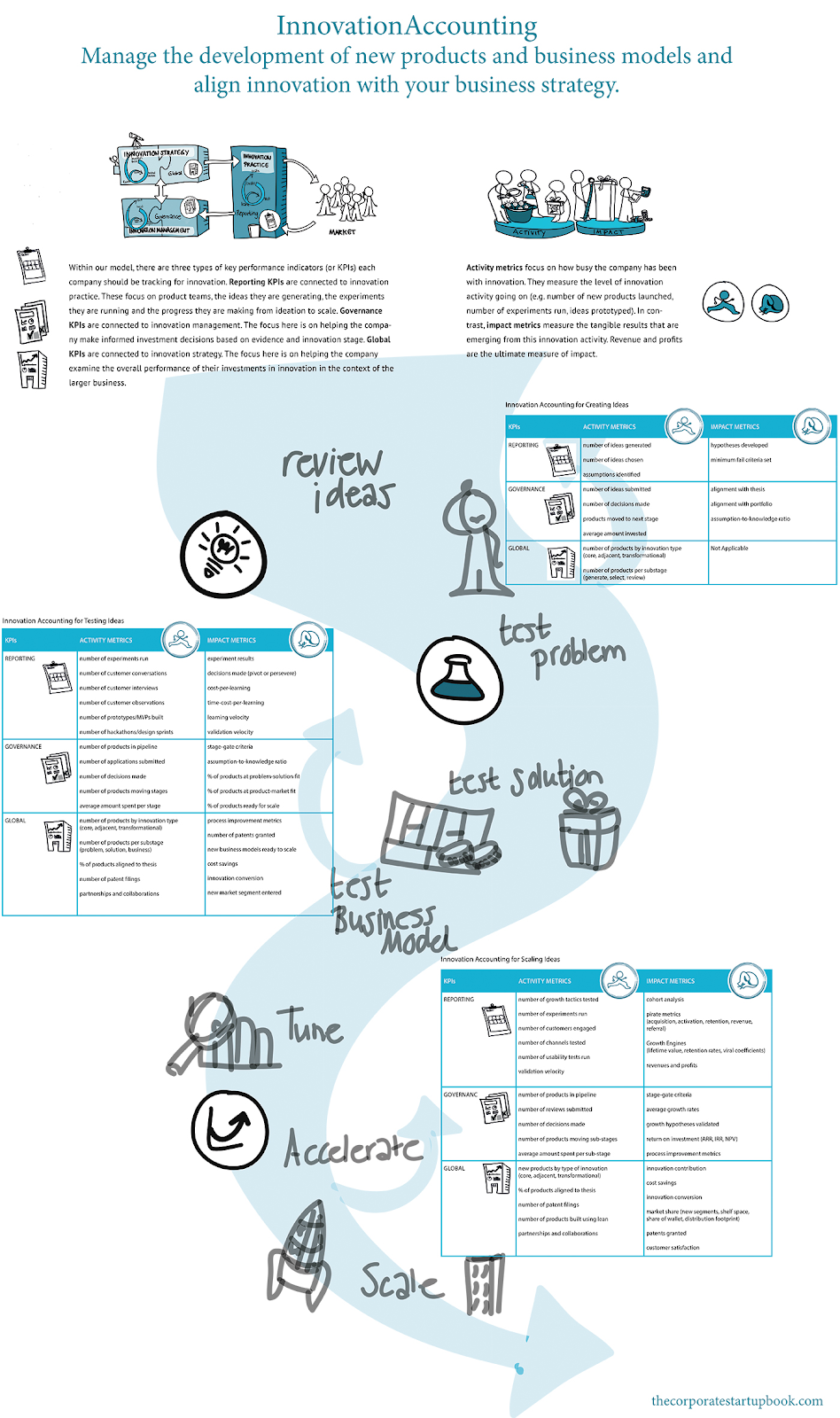

In their book ‘the corporate startup’, Dan Toma and his co-authors give some tangible, actionable metrics in what they call ‘innovation accounting’. They distinguish between three phases of a startup (idea > testing > scaling). And they use three levels of innovation metrics (reporting, governance, global). The reporting metrics are for the ‘execution level’, the innovation projects showing progress. Governance kpi’s help leaders to manage their innovation portfolio and decide where to invest. The global kpi’s help put the innovation efforts into perspective of the larger business (how do the innovations contribute to the corporate strategy / goals).

Metered funding stages risk

I love this concept. In corporate environments, people are ‘entitled’ to funding. Based on their 50 page business cases, they get funding for 2 years. No questions asked once they’re entitled to the budget. Some products even live on for years simply because the person leading it is for whatever reason entitled to run the project.

In startups, everything is about outcomes. If you don’t show results (as shown in the metrics section, the ‘outcomes’ depend on the stage your startup is in), you run out of money. Showing results means showing learning in the early stages. It means getting users and some initial income after that. And it means showing turnover and profit once the magic is working. At any stage, investors will decide whether they put their money into your startup, based on the outcomes you’ve shown (and based on your reputation with the investors).

This reduces the risk substantially. The risk is limited to the money invested at each stage. And the next investment will only happen if we’re getting more sure that the startup will produce future growth and profitability. As the likelihood of success increases, investors put in more cash.

In corporates, the managers involved in the investment want to keep control. They look at HOW the teams are spending their money. They mingle in the decisions about what features to build, what markets to serve, what people to hire. In a startup, the investor is ‘hands off’. They don’t mix in the HOW once they have made their decision to invest. They look at the outcomes to make future decisions.

In Silicon Valley, the money you raise is yours. You can spend it on what you like with minimal oversight (especially in the early stages). But Lord help you if you try to raise more money and you haven’t made any progress. Seed-stage funding provides an excellent balance between risk mitigation and freedom to innovate. The structure of the startup limits the total liability of the team to the total money raised. And it strictly limits the amount of time and energy the team has to invest in acquiring and defending its budget. But at the same time, it creates a strong incentive to keep investors informed when there’s something newsworthy to share so that they will want to continue investing and provide a positive reference to the next set of investors.

Implementing such metered funding in a corporate environment is no easy feat. Policies, governance and other regulations will all work against it. It needs strong leadership to change these structures, to defeat the regulations. I believe the ultimate structure does not need to be exactly equal to startup funding. But the staged based approach to funding instead of long term, big budgets being available to projects, will bring the right spirit. It will create accountability in the teams and focus them on showing real progress towards outcomes.

Board/investor Dynamics are key

Every startup has a board of directors and the company reports to them not on a fixed schedule but when the founders think it’s time. The review is based on actual progress, not an artificial timeline. Boards are designed to help the company think through strategic issues and whether or not to pivot. The process works because it’s linked to metered funding.

As I wrote in the previous caption, I believe in corporates, we have ‘management’ instead of ‘boards’. Management asks status updates and wants meetings with long power-point slides. Teams need to be ‘held accountable’ by management. In a startup, the board acts as ‘mentors’. If the startup wants to bounce off some ideas, they’ll speak to board members. A mentor shares experiences and insights, but does not command people, doesn’t tell them what to do.

Behind the board are the real investors. Most venture capital firms invest money of other people or institutions. The people who put their money in the fund do not interact directly with the startups. The VC has some people on the board of the startup to keep the startup on track and to gather enough data to report back to the investors.

Now in a corporate, that structure is different. The managers have kpi’s and those make them responsible for project success. Because of this, they usually control what the team is doing and mix in the strategic or even daily decision making. The problem with this is that it takes away accountability from the team. People will become dependent on the decisions from the manager. Especially if the people are officially reporting to the manager in the organisational hierarchy. And this creates a big dis-function for innovation initiatives. Entrepreneurial teams need to have the freedom to make decisions. The freedom to experiment and make decisions as they see fit.

If we want this mechanism to change, we need to change the organisational structure. Reporting lines need to be revised. Responsibilities need to be redefined. In short, the innovation teams need to be supported by management as a board would do: as mentors or advisors. They need to get freedom to innovation and experiment.